Minimum Auto Insurance Requirements by State in 2025 (Mandated Coverage by State)

Minimum auto insurance requirements by state differ, with all but New Hampshire and Virginia requiring coverage. State requirements for auto insurance always include liability coverage, and a liability-only policy averages $44 per month with top providers like Geico and State Farm.

Free Car Insurance Comparison

Compare Quotes From Top Companies and Save

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

Chris Abrams

Licensed Insurance Agent

Chris is the founder of Abrams Insurance Solutions and Marcan Insurance, which provide personal financial analysis and planning services for families and small businesses across the U.S. His companies represent nearly 100 of the top-rated insurance companies. Chris has been a licensed insurance agent since 2009 and has active insurance licenses in all 50 U.S. states and D.C. Chris works tireles...

Licensed Insurance Agent

UPDATED: Apr 17, 2025

It’s all about you. We want to help you make the right coverage choices.

Advertiser Disclosure: We strive to help you make confident auto insurance decisions. Comparison shopping should be easy. We are not affiliated with any one auto insurance provider and cannot guarantee quotes from any single provider. Our partnerships don’t influence our content. Our opinions are our own. To compare quotes from many different companies please enter your ZIP code on this page to use the free quote tool. The more quotes you compare, the more chances to save.

Editorial Guidelines: We are a free online resource for anyone interested in learning more about auto insurance. Our goal is to be an objective, third-party resource for everything auto insurance related. We update our site regularly, and all content is reviewed by auto insurance experts.

UPDATED: Apr 17, 2025

It’s all about you. We want to help you make the right coverage choices.

Advertiser Disclosure: We strive to help you make confident auto insurance decisions. Comparison shopping should be easy. We are not affiliated with any one auto insurance provider and cannot guarantee quotes from any single provider. Our partnerships don’t influence our content. Our opinions are our own. To compare quotes from many different companies please enter your ZIP code on this page to use the free quote tool. The more quotes you compare, the more chances to save.

On This Page

The minimum auto insurance requirements vary by state, determining the coverage drivers must carry to stay legal on the road. Some states require only liability insurance, while others mandate additional coverage like personal injury protection (PIP) or uninsured motorist protection.

Understanding these requirements ensures compliance with the law and financial protection in case of an accident. Failure to meet state minimums can lead to fines, license suspension, and higher insurance costs.

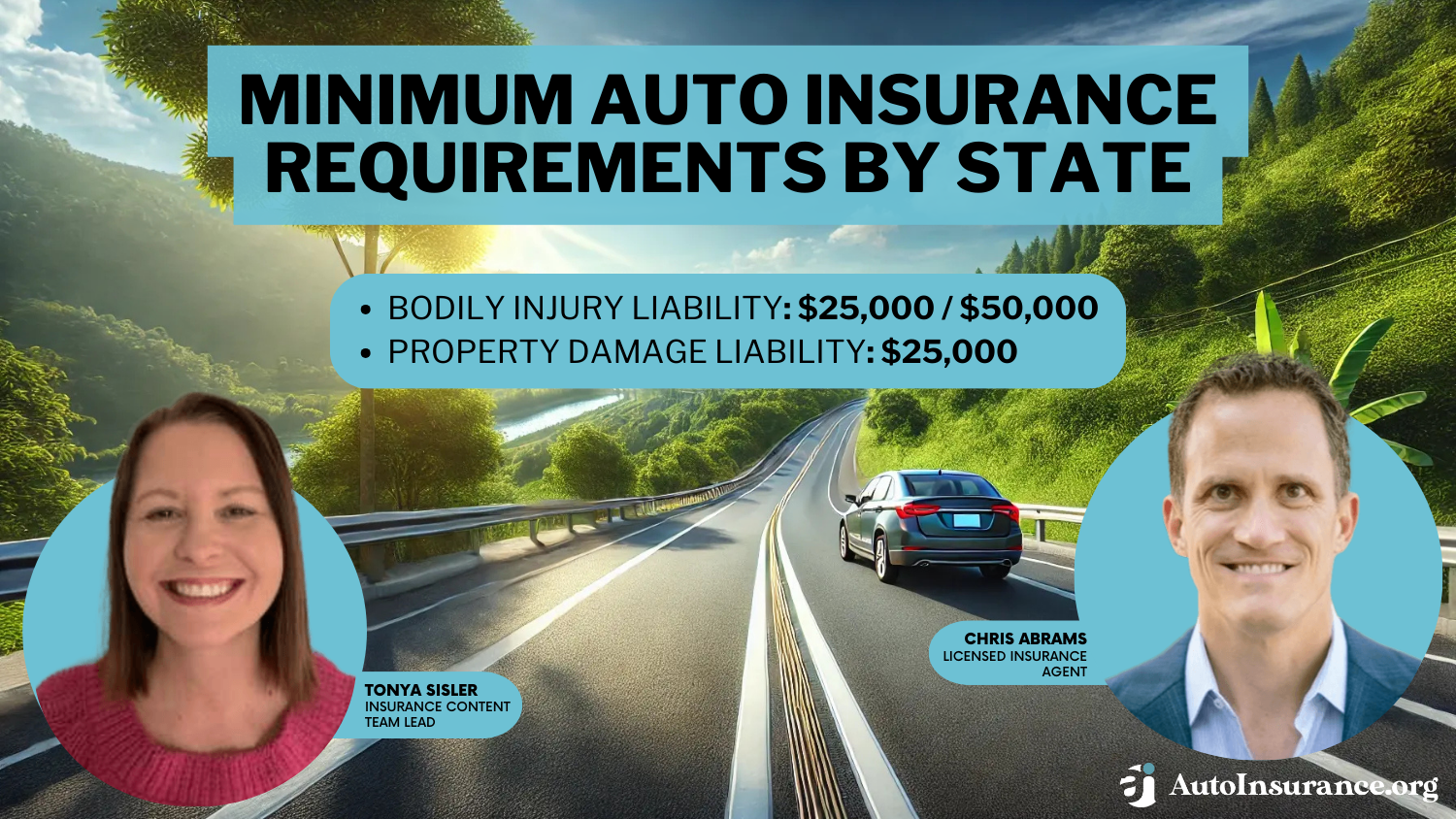

Minimum Auto Insurance Coverage Requirements & Limits

| Coverage | Limits |

|---|---|

| Bodily Injury Liability | $25,000 per person / $50,000 per accident |

| Property Damage Liability | $25,000 per accident |

Each state sets its own liability limits, typically expressed as three numbers (e.g., 25/50/25), representing bodily injury per person, bodily injury per accident, and property damage. Some states also require medical payments (MedPay) or uninsured/underinsured motorist coverage to provide extra protection.

Knowing your state’s specific requirements helps you make informed decisions about coverage beyond the legal minimums. Enter your ZIP code to compare the cheapest auto insurance companies that meet legal standards.

- Auto insurance requirements vary by state and must be met to drive legally

- Liability limits are typically shown as three numbers (e.g., 25/50/25) for coverage

- Some states require additional coverage like PIP or uninsured motorist protection

- Minimum Auto Insurance Requirements

- How to Buy a Car With a Learner’s Permit in 2025 (6 Steps to Follow)

- Minnesota Minimum Auto Insurance Requirements in 2025 (Learn What MN Requires)

- Kansas Minimum Auto Insurance Requirements in 2025 (KS Coverage Details)

- Maryland Minimum Auto Insurance Requirements in 2025 (MD Mandated Coverage)

- Hawaii Minimum Auto Insurance Requirements for 2025)(What Drivers in HI Need)

- South Dakota Minimum Auto Insurance Requirements in 2025 (SD Coverage Explained)

- New Jersey Minimum Auto Insurance Requirements for 2025 (What Drivers in NJ Need)

- Wisconsin Minimum Auto Insurance Requirements for 2025 (Basic WI Coverage Guide)

- Wyoming Minimum Auto Insurance Requirements for 2025 (Legal WY Coverage Simplified)

- Washington D.C. Minimum Auto Insurance Requirements in 2025 (Learn What DC Requires)

- Texas Minimum Auto Insurance Requirements in 2025 (Coverage You Need in TX)

- Utah Minimum Auto Insurance Requirements for 2025 (Learn What UT Requires)

- Virginia Minimum Auto Insurance Requirements in 2025 (What VA Drivers Need to Buy)

- Washington Minimum Auto Insurance Requirements for 2025 (Coverage WA Drivers Need)

- Oklahoma Minimum Auto Insurance Requirements for 2025 (What Drivers in OK Need)

- Pennsylvania Minimum Auto Insurance Requirements in 2025 (Coverage You Need in PA)

- South Carolina Minimum Auto Insurance Requirements for 2025 (See SC Policies & Limits)

- Nevada Minimum Auto Insurance Requirements in 2025 (NV Coverage Explained)

- New Hampshire Minimum Auto Insurance Requirements for 2025 (See What NH Requires Here!)

- New Mexico Minimum Auto Insurance Requirements for 2025 (NM Mandated Coverage)

- North Carolina Minimum Auto Insurance Requirements in 2025 (Coverage NC Drivers Need)

- Massachusetts Minimum Auto Insurance Requirements for 2025 (MA Mandated Coverage)

- Michigan Minimum Auto Insurance Requirements in 2025 (Coverage You Need in MI)

- Mississippi Minimum Auto Insurance Requirements for 2025 (What Drivers in MS Need)

- Missouri Minimum Auto Insurance Requirements for 2025 (Coverage MO Drivers Need)

- Montana Minimum Auto Insurance Requirements for 2025 (Coverage You Need in MT)

- Indiana Minimum Auto Insurance Requirements for 2025 (What IN Drivers Need)

- Kentucky Minimum Auto Insurance Requirements in 2025 (Coverage You Need in KY)

- Louisiana Minimum Auto Insurance Requirements in 2025 (See What All LA Drivers Need)

- Connecticut Minimum Auto Insurance Requirements in 2025 (CT Mandated Coverage)

- Florida Minimum Auto Insurance Requirements in 2025 (FL Coverage Guide)

- Georgia Minimum Auto Insurance Requirements in 2025 (Coverage GA Drivers Need)

- Idaho Minimum Auto Insurance Requirements (What ID Drivers Need in 2025)

- Arkansas Minimum Auto Insurance Requirements in 2025 (AR Mandated Coverage)

- Colorado Minimum Auto Insurance Requirements in 2025 (Everything CO Drivers Should Know)

- Alabama Minimum Auto Insurance Requirements in 2025 (What AL Drivers Need)

- Alaska Minimum Auto Insurance Requirements in 2025 (What AK Drivers Need to Buy)

- Arizona Minimum Auto Insurance Requirements in 2025 (What AZ Drivers Should Know)

- Auto Insurance Laws

Minimum Coverage Requirements by State & What They Cover

Do all states require auto insurance? Nearly every state requires drivers to carry a certain amount of car insurance before they can register a car or drive on public roads.

States that require auto insurance want to protect people from accidents they did not cause. When you carry liability auto insurance, you’ve guaranteed your ability to pay for damage you might cause in an accident.

This is why most states only require auto liability insurance — you can choose not to protect your own car, but other drivers shouldn’t be financially responsible for damage you cause. You can check the required minimum auto insurance by state below.

Minimum Car Insurance Requirements by State

| State | Liability Coverage | UM/UIM | PIP / MedPay | State Resources |

|---|---|---|---|---|

| Alabama | 25/50/25 | Not required | Not required | Alabama DOR |

| Alaska | 50/100/25 | Not required | Not required | Alaska DMV |

| Arizona | 25/50/15 | Not required | Not required | Arizona DIFI |

| Arkansas | 25/50/25 | Not required | PIP $5,000 (medical) | Arkansas Insurance Dept. |

| California | 30/60/15 | Not required | Not required | California DMV |

| Colorado | 25/50/15 | Not required | Not required | Colorado DMV |

| Connecticut | 25/50/25 | Required (25/50) | Not required | Connecticut Insurance Dept. |

| Delaware | 25/50/10 | Not required | PIP $15,000/$30,000 | Delaware DMV |

| Florida | 10/20/10* | Not required | PIP $10,000 | Florida HSMV |

| Georgia | 25/50/25 | Not required | Not required | Georgia Motor Vehicles |

| Hawaii | 20/40/10 | Not required | PIP $10,000 | Hawaii DCCA |

| Idaho | 25/50/15 | Not required | Not required | Idaho DOI |

| Illinois | 25/50/20 | Required (UM 25/50) | Not required | Illinois Vehicle Services |

| Indiana | 25/50/25 | Not required | Not required | Indiana DOI |

| Iowa | 20/40/15 | Not required | Not required | Iowa Insurance Division |

| Kansas | 25/50/25 | Required (25/50) | PIP (min. $4,500 med, etc.) | Kansas Division of Vehicles |

| Kentucky | 25/50/25 | Required (25/50) | PIP $10,000 | Kentucky DMV |

| Louisiana | 15/30/25 | Not required | Not required | Louisiana DOI |

| Maine | 50/100/25 | Required (50/100) | MedPay $2,000 | Maine BOI |

| Maryland | 30/60/15 | Required (30/60/15) | PIP $2,500 | Maryland MVA |

| Massachusetts | 20/40/5 | Required (20/40) | PIP $8,000 | Massachusetts DOI |

| Michigan | 50/100/10 | Not required | PIP (required – choice of limits) | Michigan DIFS |

| Minnesota | 30/60/10 | Required (25/50) | PIP $40,000 | Minnesota Motor Vehicle |

| Mississippi | 25/50/25 | Not required | Not required | Mississippi Insurance Dept. |

| Missouri | 25/50/25 | Required (25/50) | Not required | Missouri Dept. of Revenue |

| Montana | 25/50/20 | Not required | Not required | Montana MVD |

| Nebraska | 25/50/25 | Required (25/50) | Not required | Nebraska DMV |

| Nevada | 25/50/20 | Not required | Not required | Nevada Division of Insurance |

| New Hampshire | 25/50/25 | Required (25/50) | Not required | New Hampshire Insurance Dept. |

| New Jersey | 25/50/25 | Required (25/50) | PIP $15,000 | New Jersey MVC |

| New Mexico | 25/50/10 | Not required | Not required | New Mexico MVD |

| New York | 25/50/10 | Required (25/50) | PIP $50,000 | New York DMV |

| North Carolina | 30/60/25 | Required (30/60) | Not required | North Carolina DMV |

| North Dakota | 25/50/25 | Required (25/50) | PIP $30,000 | North Dakota Insurance Dept. |

| Ohio | 25/50/25 | Not required | Not required | Ohio BMV |

| Oklahoma | 25/50/25 | Not required | Not required | Oklahoma Insurance Dept. |

| Oregon | 25/50/20 | Required (25/50) | PIP $15,000 | Oregon DMV |

| Pennsylvania | 15/30/5 | Not required | PIP $5,000 | Pennsylvania DMV |

| Rhode Island | 25/50/25 | Not required | Not required | Rhode Island DMV |

| South Carolina | 25/50/25 | Required (25/50) | Not required | South Carolina DOI |

| South Dakota | 25/50/25 | Required (25/50) | Not required | South Dakota Dept. of Labor |

| Tennessee | 25/50/15 | Not required | Not required | Tennessee DOR |

| Texas | 30/60/25 | Not required | PIP $2,500 (unless waived) | Texas DOI |

| Utah | 25/65/15 | Not required | PIP $3,000 | Utah DMV |

| Vermont | 25/50/10 | Required (25/50) | Not required | Vermont DMV |

| Virginia | 25/50/20 | Required (25/50/20) | Not required | Virginia DMV |

| Washington | 25/50/10 | Not required | Not required | Washington Dept. of Licensing |

| West Virginia | 25/50/25 | Required (25/50) | Not required | West Virginia DMV |

| Wisconsin | 25/50/10 | Required (25/50) | Not required | Wisconsin DOT |

| Wyoming | 25/50/20 | Not required | Not required | Wyoming DOT |

Does every state have the same requirements for coverage? Most states require a minimum amount of liability, while several others include personal injury protection, medical payments, or uninsured/underinsured motorist as part of the coverage requirements.

Your state’s minimum car insurance is the cheapest option for coverage, but it comes with a risk. You’ll have to pay for any repairs your car needs from your own pocket. You’ll also have to pay for damage you cause in an accident if your liability coverage runs out.

You can avoid financial hardship by buying more liability coverage than your state requires and getting coverage for your car.

Types of Auto Insurance Coverages Required

You might have noticed several types of coverage listed as state requirements for car insurance. Insurance laws might be confusing, but you can explore what they mean below:

- Liability: Liability insurance pays for damage you cause in an accident. The amount of minimum liability insurance you need varies by state. To get the cheapest liability insurance, consider factors like your driving history, the state you live in, and discounts (such as bundling with home insurance or safe driver discounts).

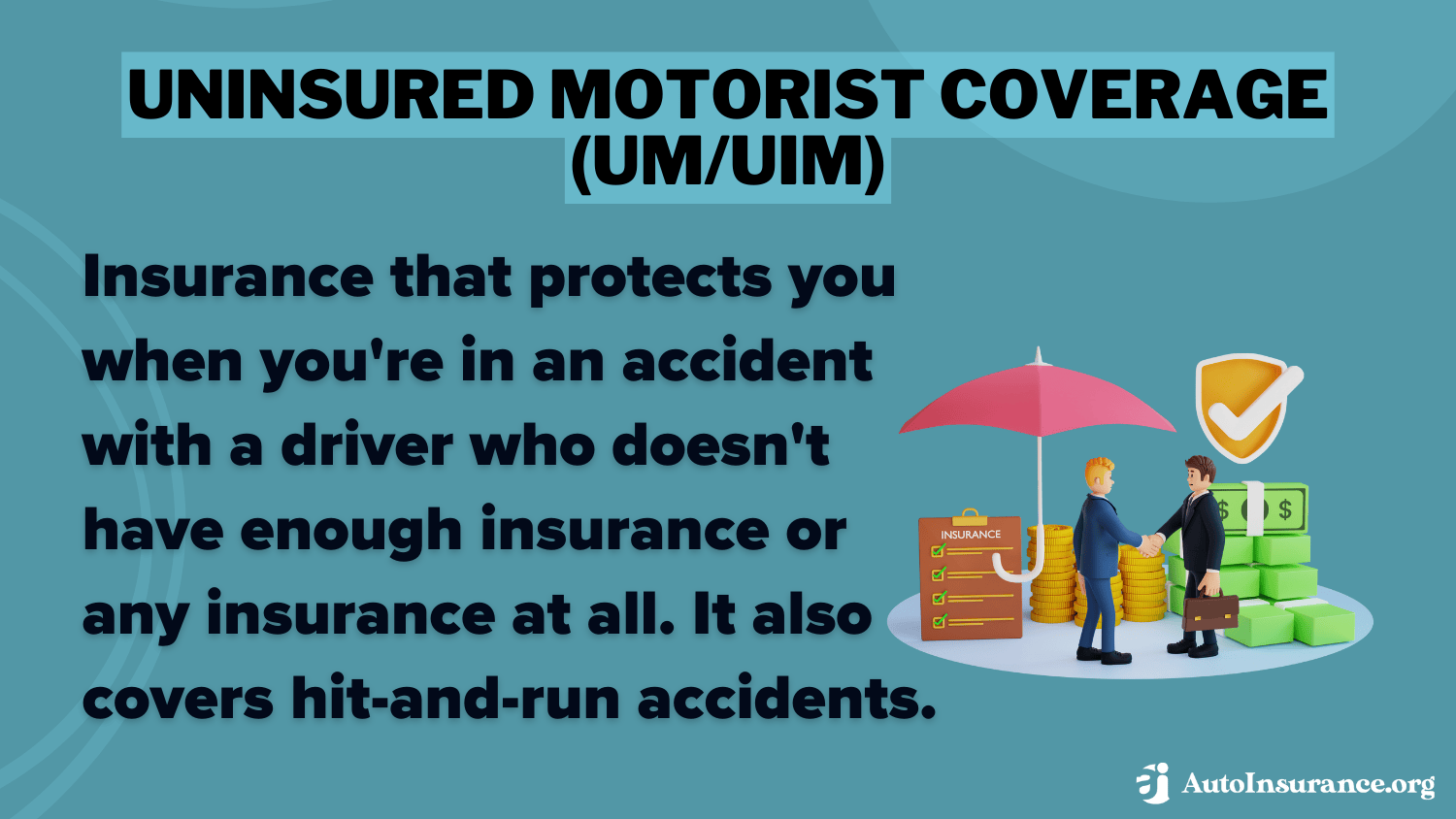

- Uninsured/underinsured motorist (UM/UIM): UM/UIM insurance protects you from drivers who don’t have adequate insurance. It also covers you if you’re the victim of a hit-and-run.

- Personal injury protection (PIP): Personal injury protection coverage covers medical expenses related to injuries you or your passengers sustain in an accident. It also covers funeral costs, lost wages, and other related expenses.

- Medical payments: Similar to PIP, medical payments insurance covers injuries after an accident. Unlike PIP, it doesn’t cover lost wages and related expenses — it only pays for direct medical expenses.

Although minimum car insurance is your cheapest option, many drivers elect for more coverage to ensure their cars are well protected. Two of the most popular coverages that can complete your car’s protection are comprehensive and collision car insurance.

Collision insurance pays for repairs to your vehicle after an at-fault accident. Comprehensive auto insurance covers damage from other events, like fire, weather, theft, vandalism, and animal contact.

Many car loan lenders and lease holders require drivers to get full coverage, which includes comprehensive and auto collision insurance. Although these coverages are valuable, they are not required by any state law.

States That Don’t Require Car Insurance

There are only a few states where car insurance is not required. The first state that doesn’t require car insurance is New Hampshire – it only requires drivers to prove their ability to pay for damage they cause in an accident. If you can’t demonstrate your financial ability, New Hampshire auto insurance requirements are 25/50/25 plan for liability coverage.

While New Hampshire auto insurance laws don’t list an exact amount that proves your financial ability to pay for damages, it should at least be enough to equal the liability requirements. If you drive without being financially able, you can lose your license and have your registration suspended.

Although New Hampshire doesn’t require drivers to carry car insurance, the state can require people to buy insurance after violations like DUIs. The other state that doesn’t require car insurance is Virginia. If you choose not to buy Virginia auto insurance, you’ll have to pay an uninsured motorist fee of about $500 a year.

Skipping car insurance leaves you vulnerable to financial hardship after an accident. If you’re wondering how to get insurance, the minimum requirements for auto insurance in Virginia are 25/50/20 for liability coverage. Since car insurance in Virginia usually costs about the same as the uninsured motorist fee, your best bet is usually buying coverage.

Some states that don’t require car insurance let drivers skip coverage by making a large deposit with the DMV, typically ranging from $25,000 to $115,000. However, this option leaves you without the essential protection that car insurance provides.

Free Auto Insurance Comparison

Enter your ZIP code below to view companies that have cheap auto insurance rates.

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

Cheapest Car Insurance by State

In the United States, each state has its own auto insurance regulations. Auto insurance laws by state vary in how much coverage they require — some states demand the bare minimum car insurance while others have much stricter laws. No matter what the laws are in your state, if your budget is tight, it’s best to get cheap car insurance within the state minimum.

18,154 reviews

18,154 reviewsCompany Facts

Min. Coverage by State

A.M. Best Rating

Complaint Level

Pros & Cons

18,154 reviews 13,283 reviews

13,283 reviewsCompany Facts

Min. Coverage by State

A.M. Best Rating

Complaint Level

Pros & Cons

13,283 reviews 19,116 reviews

19,116 reviewsCompany Facts

Min. Coverage by State

A.M. Best Rating

Complaint Level

Pros & Cons

19,116 reviewsIf minimum coverage sounds right for you, you should still compare state minimum car insurance quotes with multiple companies to find the best price. Although minimum insurance is the cheapest option, you’ll see different rates based on your unique circumstances.

Penalties for Driving Without Insurance by State

Driving without insurance can result in serious consequences, with penalties differing from state to state. Understanding these penalties is crucial to avoid costly mistakes and ensure you’re always compliant with the law.

- Fines: Many states impose hefty fines on drivers without the required auto insurance. These fines can range from a few hundred dollars to over $1,000, depending on the state and the severity of the violation. Some states may also impose additional fines for each day the driver remains uninsured after the violation.

- License Suspension: In many states, your driver’s license may be suspended or revoked if you are caught driving without insurance. This means you will not be able to legally drive until your license is reinstated, which may require proof of insurance and the payment of additional fees.

- Vehicle Registration Suspension: If you’re caught driving without insurance, your vehicle registration may be suspended. Without a valid registration, you may be unable to legally drive your vehicle, and the process to reinstate your registration can be both costly and time-consuming.

- Impounding of the Vehicle: In some states, your vehicle may be impounded if you’re caught driving without insurance. To recover your vehicle, you may have to pay impound fees and registration fees and possibly provide proof of insurance.

- Higher Insurance Premiums: Once you’ve been caught driving without insurance, you are likely to face higher insurance premiums. Insurance companies consider uninsured drivers to be high-risk and may charge significantly more to cover them.

- Court Appearances: Depending on the state, drivers caught without insurance may be required to appear in court. This can result in additional legal fees and severe penalties like probation.

- Increased Liability: If you cause an accident without insurance, you’ll be personally responsible for any damages or injuries. This can result in significant financial strain, as you’ll likely have to cover medical bills, vehicle repairs, and legal fees out of your own pocket. Additionally, you may face lawsuits from the other party involved in the accident.

- Possible Jail Time: In rare cases, repeat offenders or those caught driving without insurance in conjunction with other legal violations (such as DUI) may face jail time. This is less common but still a potential consequence in extreme cases.

Here’s a table showing the penalties for driving without insurance in each state. Remember, these penalties can vary greatly based on where you live:

State-Specific Penalties for Driving Without Insurance

| State | Fine | License Suspension | SR-22 Requirement | Additional Penalties |

|---|---|---|---|---|

| Arizona | $500–$1,000 | Yes (up to 1 year) | Yes | Vehicle registration suspension |

| California | $100–$500 | Possible | Yes (if convicted) | Vehicle impoundment |

| Florida | $150–$500 | Yes (up to 3 years) | Yes | Registration suspension |

| Georgia | $200–$1,000 | Yes (up to 90 days) | Yes | Possible jail time |

| Illinois | $500+ | Yes (minimum 3 months) | Yes | Additional reinstatement fees |

| Michigan | $200–$500 | Yes | Yes | Possible jail time |

| New York | Up to $1,500 | Yes (up to 1 year) | Yes | $750 civil penalty |

| Ohio | $100–$600 | Yes | Yes | Impoundment for repeat offenses |

| Pennsylvania | $300 | Yes (3 months) | No | Registration suspension |

| Texas | $175–$350 (1st offense) | Possible | Yes | Higher fines for repeat offenses |

It’s essential to have at least the minimum required auto insurance coverage in your state to avoid these penalties. If you can’t afford standard insurance rates, you may want to look into state-sponsored programs or compare insurance quotes to find the most affordable option.

Minimum Car Insurance Coverage by State and Policy Differences

Every state has its own set of rules for driving and minimum insurance coverage. Liability is the minimum requirement in most states. Is there a difference in auto insurance state minimum coverage between states?

Min. Coverage Auto Insurance Monthly Rates by State

| State | Rates |

|---|---|

| Alabama | $74 |

| Alaska | $106 |

| Arizona | $89 |

| Arkansas | $68 |

| California | $132 |

| Colorado | $94 |

| Connecticut | $112 |

| Delaware | $91 |

| Florida | $138 |

| Georgia | $82 |

| Hawaii | $115 |

| Idaho | $78 |

| Illinois | $97 |

| Indiana | $83 |

| Iowa | $72 |

| Kansas | $76 |

| Kentucky | $81 |

| Louisiana | $121 |

| Maine | $87 |

| Maryland | $102 |

| Massachusetts | $127 |

| Michigan | $108 |

| Minnesota | $84 |

| Mississippi | $71 |

| Missouri | $90 |

| Montana | $79 |

| Nebraska | $74 |

| Nevada | $96 |

| New Hampshire | $92 |

| New Jersey | $118 |

| New Mexico | $86 |

| New York | $135 |

| North Carolina | $93 |

| North Dakota | $70 |

| Ohio | $79 |

| Oklahoma | $74 |

| Oregon | $99 |

| Pennsylvania | $104 |

| Rhode Island | $113 |

| South Carolina | $87 |

| South Dakota | $72 |

| Tennessee | $92 |

| Texas | $98 |

| Utah | $84 |

| Vermont | $91 |

| Virginia | $95 |

| Washington | $109 |

| West Virginia | $80 |

| Wisconsin | $81 |

| Wyoming | $73 |

| Slidell | $76 |

| Thibodaux | $66 |

| West Monroe | $65 |

There is a difference in the amount of liability coverage that each driver is required to carry between all of the states.Every state sets its own rules for driving and how people must conduct themselves on public roads.

This means that each state has the right to set the amount of insurance coverage that people must have at as high or as low an amount as they believe is necessary.

Read More: Auto Insurance Rates by State

Bodily Injury Liability Auto Insurance

The type of liability coverage that most states require that drivers purchase is bodily injury liability and property damage liability coverage. Bodily injury liability insurance consists of two different numbers.

The first number is the amount of coverage that drivers must have in the event that they are the cause of an accident that results in bodily injuries to one person. For example, in one state, for one person hurt in a car collision, the one who caused the accident must have purchased a policy that offers $15,000 to pay the injured party’s medical bills or funeral expenses.

The second number related to bodily injury liability coverage is the amount of money that people must have for everyone hurt in the accident that the driver has caused. In the state above, drivers must have bought a policy that will pay $30,000 total for everyone hurt in the accident.

Property Damage Liability Auto Insurance

The third number is associated with property damages. The property damage liability coverage is the amount of money that drivers must be prepared to pay for property repairs, such as for:

• Cars

• Utility Poles

• Damaged landscaping

• Livestock that has been injured or killed

• Damages to buildings and houses

In the example, property damage liability is required to be $10,000 under these policies. The minimum property damage limits by state are 15/30/10.

Free Auto Insurance Comparison

Enter your ZIP code below to view companies that have cheap auto insurance rates.

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

Other Coverage Options to Consider in Each State

Many drivers choose to enhance their protection with additional coverage options. These extra options can provide more comprehensive financial security in case of accidents, natural disasters, or other unexpected events. Depending on their state’s requirements and personal needs, drivers should consider these common types of coverage.

- Comprehensive Coverage: This covers damages to your car not involving a collision, such as theft, vandalism, fire, or weather-related incidents. When to Consider: Ideal for drivers who want protection from a wide range of risks, especially in high-risk areas.

- Collision Coverage: Pays for damage to your vehicle after an accident, regardless of who is at fault. When to Consider: Recommended for drivers with newer or high-value cars to avoid the cost of repair or replacement after a crash.

- Personal Injury Protection (PIP): PIP insurance covers medical expenses for injuries sustained by the driver and passengers, as well as lost wages and other out-of-pocket costs. When to Consider: Required in no-fault states and recommended for those wanting coverage for medical costs, even if not at fault.

- Uninsured/Underinsured Motorist (UM/UIM): Protects against drivers who don’t have enough or any insurance to cover your costs after an accident. When to Consider: Essential in states with high uninsured motorist rates, especially for drivers who want protection in a hit-and-run.

- Medical Payments Coverage (MedPay): Covers medical expenses for you and your passengers, regardless of who caused the accident. When to Consider: Ideal for drivers who want additional protection for medical bills without the extensive coverage of PIP.

- Roadside Assistance: Provides help with emergencies like flat tires, breakdowns, or dead batteries. When to Consider: Great for drivers who often travel long distances or live in areas where help may be slow to arrive.

- Rental Car Reimbursement: Pays for a rental car while your car is being repaired after an accident. When to Consider: Recommended for drivers who rely on their vehicle for daily transportation and want to avoid disruption.

- Gap Insurance: Covers the difference between what you owe on your vehicle loan and its current market value if it’s totaled in an accident. When to Consider: Ideal for drivers with new cars or those still paying off their vehicle loan who want to avoid paying out-of-pocket.

Drivers should review their coverage options to ensure full protection, as each state has its own requirements. Extra coverage can provide peace of mind in case of an accident or unexpected events. Depending on your driving habits, vehicle type, and the state you live in, it may be worth exploring these coverage options to avoid gaps in protection.

The Basic and Standard Policies

When people opt to buy just the liability coverage required in tort states, they are purchasing the basic policy.

State minimum insurance may not cover all accident costs, leaving you with hefty bills. Smart drivers choose extra coverage for better protection.Schimri Yoyo Licensed Agent & Financial Advisor

Every auto insurance company is required to sell packages that include at least the state’s minimum requirements.

The other choice people have when they wish to purchase more than just the minimum requirements is to buy a standard policy.

With the standard policy, they will have the liability coverage they need in tort states, plus the extra coverage they must have in no-fault states and the optional coverage they choose.

Uninsured/Underinsured Motorist Coverage

Another reason that drivers in some states will pay for more coverage than in other states is that some states require that their drivers purchase more than just liability.

For example, a state may obligate drivers to have uninsured/underinsured motorist insurance.

By mandating that all drivers purchase liability coverage, the states have set out to decrease instances when drivers cannot take financial responsibility for the damages they cause when they drive recklessly.

When people do not do this and drive uninsured or underinsured, the injured drivers have the recourse of obtaining payment for their bills with their uninsured motorist coverage.

Making Auto Insurance Affordable

If drivers have a difficult time affording their insurance policies, they may decide that they would like to purchase the basic policy.

With the least amount of insurance, these drivers will obtain the lowest prices for their auto insurance coverage.

Although purchasing the state’s minimum requirements will only keep drivers from receiving penalties and possibly losing their licenses, it will not be enough coverage to keep them from losing their savings to the repairs needed on their own vehicles and their medical bills.

Read More: How to Lower Your Auto Insurance Rates

Auto Insurance Coverage Across the U.S.

States require auto insurance to protect both car owners and the public from financial loss in accidents. Without it, victims would bear medical and repair costs. Insurance ensures the at-fault driver isn’t fully liable, covering damages per policy terms.

The insured person would be liable only for their auto insurance deductible, which is the amount they have to pay before the insurance company begins to make the remaining payments.

Automobile insurance, therefore, provides the insured person with the safety of knowing that as long as they pay the insurance premiums, the insurance company will agree to pay for damages that are specified in the insurance policy.

Free Auto Insurance Comparison

Enter your ZIP code below to view companies that have cheap auto insurance rates.

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

Understanding Auto Insurance Minimums by State

Most states require a person owning a car to have minimum car insurance coverage through a licensed insurance company that provides automobile coverage. There are two areas that must be covered by the law:

- Bodily injury liability: This part of the insurance policy provides coverage for any medical bills, pain, and suffering, or other medically necessary expenses resulting from a car accident.

- Property damage liability: Property damage liability helps pay for damage to another person’s car and other property damaged in the accident. If the person who is insured is found to be at fault for an accident, they would be responsible, through their insurance company, for the cost of damage repair. Read more about the best property damage liability (PDL) auto insurance companies.

Here is how minimum auto insurance coverage works. There are generally three numbers that a person will see when looking at state-mandated minimum automobile insurance coverage. The numbers appear as 25/50/30. These numbers refer to bodily injury liability and property damage liability in dollar amounts.

- The 25 refers to the fact that the insurance must provide up to $25,000 coverage for the first person filing an injury claim in an accident

- The second number, 50, is the maximum amount of insurance coverage for any personal injury claims filed by the insurer or any other person involved in an accident, or $50,000

- The third number, 20, means that the auto insurance coverage must provide a maximum of $20,000 to pay for property damage

This minimum coverage may seem to provide total coverage; however, it depends on how many people were injured in the accident.

If three or more people sustained injuries and the total amount of medical expenses equaled more than $50,000, the insured person could then be personally sued to recover any remaining medical bills as a result of the accident.

What's an at-fault accident🚘? Can you be at fault if you live in a no-fault state🇺🇸? https://t.co/27f1xf131D has the info you need to clear things up. Find out what you need here👉: https://t.co/LWLZy8nIWK pic.twitter.com/SuFnzANtes

— AutoInsurance.org (@AutoInsurance) September 4, 2023

If all the people involved in the accident did not incur costs equaling the $50,000 then everyone’s medical bills would be covered by the insurance company.

Depending on the severity of the accident, the person at fault for the accident could potentially find themselves being sued for medical expenses that exceed state-mandated minimum coverage amounts.

Finding Cheap Car Insurance Minimums by State

When looking into the minimum auto insurance requirements by state, it is always recommended that a person interested in car insurance contact several automobile insurance companies to compare cheap auto insurance quotes and auto insurance types. This will help you find the best auto insurance company for you.

Even when purchasing state minimum required coverage, comparison shopping for the required auto insurance makes sense as costs may differ depending on the insurance company. Make sure to compare the best car insurance rates by using our free insurance comparison tool below.

Frequently Asked Questions

What states don’t require car insurance?

New Hampshire and Virginia are the only states without mandatory car insurance coverage. Instead, drivers must pay for any expenses they cause in an at-fault accident.

What’s the legal minimum insurance coverage you must have to drive on public roads?

Minimum auto insurance requirements refer to the legally mandated minimum amount of insurance coverage that drivers must carry in a specific state. These requirements vary from state to state and typically include liability coverage for bodily injury and property damage.

Why do states have minimum auto insurance requirements?

State requirements for car insurance exist to ensure that drivers have a basic level of financial responsibility in case they cause accidents or damage to others. These requirements help protect individuals and property by ensuring that there is some form of insurance coverage available to compensate for injuries or damages caused by at-fault drivers.

How do minimum auto insurance requirements vary by state?

The state-required insurance varies in terms of the specific coverage amounts and types mandated. Each state sets its own minimum requirements based on various factors, including accident statistics, population density, and local insurance regulations.

Is car insurance required in all states?

Do you have to have auto insurance in every state? Almost every state does require car insurance, but each state has its own set of minimum auto insurance requirements. The coverage amounts and types mandated can differ significantly. It’s essential for drivers to understand the specific requirements in the state where they reside or plan to drive.

How can I find out the minimum auto insurance requirements in my state?

To find out what type of car insurance is required in your state, you can visit your state’s Department of Motor Vehicles (DMV) website or contact them directly. The DMV or the state insurance department can provide you with the most accurate and up-to-date information regarding the minimum coverage requirements.

Can I purchase more than the minimum required auto insurance coverage?

Yes, you can and often should purchase more than the minimum required auto insurance coverage. While the minimum coverage satisfies the legal requirement, it may not provide adequate protection in the event of a significant accident. It’s generally recommended to consider higher liability limits, as well as additional coverages such as collision, comprehensive, and uninsured/underinsured motorist coverage, to ensure comprehensive protection.

Read More: When to Buy More Than Minimum Auto Insurance

How many states require car insurance?

You may be wondering what states require car insurance. In the US, every state does require car insurance. The only two states where car insurance is not mandatory are Virginia and New Hampshire.

Do any states not require car insurance?

New Hampshire and Virginia are the only two states that don’t require car insurance.

How many states require auto insurance?

Car insurance is required in 48 states.

Which type of auto coverage is required by nearly every state in the country?

So, what type of auto insurance does the state require car owners to purchase? Nearly every state in the US requires drivers to have liability insurance coverage.

What are the state minimum limits for auto insurance?

The minimum state standards for insurance vary by state. For example, Alabama minimum car insurance requirements are 25/50/25 while Iowa auto insurance requirements are 20/40/15.

Wyoming auto insurance requirements are 25/50/20, while Wisconsin car insurance requirements are 25/50/10.

What states do not need car insurance?

In the United States, Virginia and New Hampshire are the only two states where you don’t need car insurance. Enter your ZIP code for more information on your state’s insurance laws.

What is the purpose of minimum insurance coverage?

Minimum coverage helps protect drivers who are at fault in an accident from facing a financial burden due to others’ medical expenses, lost wages, and property damage. Read our “Does auto insurance cover private property?” to learn more about coverage details.

Does New Hampshire require car insurance?

New Hampshire does not require drivers to have car insurance as long as they can demonstrate the ability to meet New Hampshire Motor Vehicle Financial Responsibility Requirements in the event of an at-fault accident.

What are the minimum car insurance requirements in Wisconsin?

According to Wisconsin car insurance laws, drivers are required to carry at least 25/50/10 of liability coverage.

Free Auto Insurance Comparison

Enter your ZIP code below to view companies that have cheap auto insurance rates.

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

Chris Abrams

Licensed Insurance Agent

Chris is the founder of Abrams Insurance Solutions and Marcan Insurance, which provide personal financial analysis and planning services for families and small businesses across the U.S. His companies represent nearly 100 of the top-rated insurance companies. Chris has been a licensed insurance agent since 2009 and has active insurance licenses in all 50 U.S. states and D.C. Chris works tireles...

Licensed Insurance Agent

Editorial Guidelines: We are a free online resource for anyone interested in learning more about auto insurance. Our goal is to be an objective, third-party resource for everything auto insurance related. We update our site regularly, and all content is reviewed by auto insurance experts.